In Spain & Italy the wheat harvest is about 75% complete, although rain delayed proceedings in Italy, and the combines have started to roll in France, Germany & Poland. In Spain yields are said to be exceptional, similarly Morocco and Algeria are said to have had good harvests, so that France may export less this year. The wheat problem in China (discussed last week) means that global wheat prices have been supported by continual Chinese purchases, and overall the global Supply & Demand has changed from surplus to in-balance. Therefore only competition from barley or maize has the potential to push wheat prices higher or lower, so that means we are back to watching the weather and monitoring harvest reports. Currently the harvests in the northern hemisphere look promising, with no crises on the horizon. The Black Sea harvest is also 75% complete.

UK farmers are not selling wheat forward, probably because last year they sold more wheat than harvested, so with burnt fingers are waiting until the wheat is in the barn. UK wheat is about £168 delivered to the mill.

Ensus, the three-times in three years mothballed biofuel plant, which cost £250m to build, has been sold to German bioethanol company for just £11.7m. Presumably the new owners will want it to eat wheat again; it is capable of consuming 10% of this years’ 12mt crop which is not-so-good for livestock farmers. Ensus & Vivergo together could eat 2.4mt of feed wheat, so the price direction will be defined by the quality and quantity of this year’s crop.

Brazil is the largest producer of sugar in the world. It produced 2.4mt of sugar in the first two weeks of July and expects to produce 14mt during the three months July-Sep. The queue of waiting ships today is numbered in hundreds, each with an average waiting time of 34 days; so ships waiting to load soya and maize are now competing with sugar.

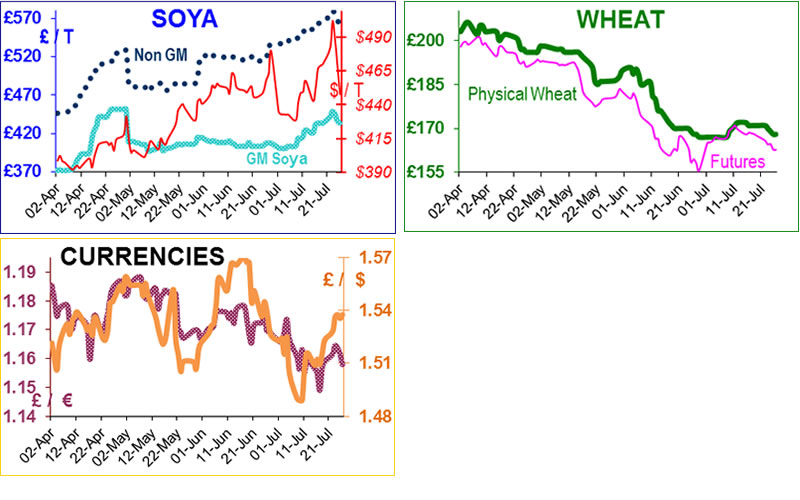

In the UK soya supplies are so tight that some importers have run out of stocks, so prices remain high. NonGM soya has not been available since 14th June.

US soya bean meal futures hit a high of $521/short ton on Tuesday, at which time GM soya was being sold ex UK port at £435/t, £20/t more than a week ago. In ball park terms, it then finished limit down $20/t on Tuesday, Wednesday and Thursday when it was trading at $447/short ton, ie $74 change in 3 days! The last time that soya fell by its daily trading limit was in February 2011.

It would appear that the very high prices were the stimulus for end-of-year market-opportunist US soya farmers to open their barn doors. The flood of soya caused the funds to sell in style and the market collapsed because a) the trade realised there was plenty of soya and b) there were few buyers because most of the crushers had cover for the four weeks to harvest. There was also a rumour that China was going to release 3mt of soya from its reserves. The weather forecast for the next two weeks is perfect for the soya crop.

The elephant in the room is the funds. Investment funds which traditionally take long positions on commodities, have taken a short position on maize, and on one day this week sold 18000 contracts.

The funds have generally lost money on commodities every month since January because their long-only premise was based on the assumption that prices would continue to rise because of population growth and the BRIC’s hunger for raw materials. This simplistic view meant that the value of the average fund diminished by 3.58% since Jan 1st. However it would be difficult to be bullish in light of the latest USDA estimate of US maize production of a record 354mt, 80mt more than last year.