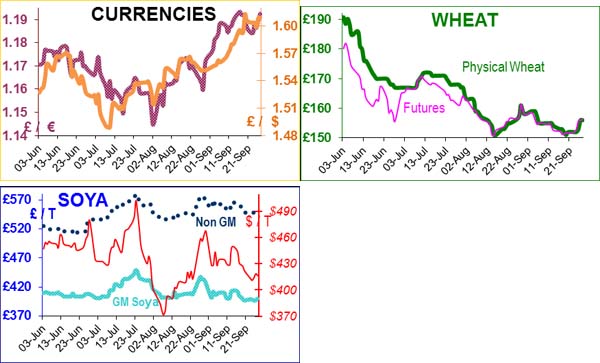

November wheat futures prices hit a bottom of £150.75 in mid-August and again touched £150.00 in mid-September, otherwise the average price during August and September has been about £156.

In essence there is good support at £150, and UK arable farmers seem to see this as a minimum price and are in no rush to sell, so wheat prices lifted this week as the trade had to scrabble to find wheat to supply the feed trade for October. UK Nov futures wheat is trading at about £155, and EU wheat is about £161. UK and EU wheat seems to be of good quality, with much of the EU wheat being of milling quality to the point that the EU may be short of feed wheat. However that shortage is being made up with plenty of barley and maize, both of which will feature in EU feed formulations this year.

The EU maize harvest has started, and globally it is believed that eight of the top ten maize producers will have record crops this year, so Reuters believes the world will produce 949mt of maize this year (942mt last year). The Ukraine is expected to produce 60mt of cereals this year (46mt last year). Black Sea maize prices are currently more competitive than EU production. Four days of frosts prior to the imminent Argentinean wheat harvest supported prices this week, but local farmers believe this year’s yields will still exceed last year.

Australia’s wheat harvest looks on track too. Overall there seems to be a plentiful sufficiency of cereals for this harvest year.

Soya beans are a different story. The low old crop carry-out of 125m bushels this year lifted prices in recent months, and the lack of moisture will adversely affected the new crop, so the USDA reduced the anticipated yields from 42.6b/a to 41.2b/a and predicted next year’s carry-out to be 150mb, only 25mb more than this year. Currently US soya stocks are so low that pressure is building on South America to surrender their stocks.

Brazil has about 20mt surplus, but is still suffering from export constipation, which is pressurising prices and another big crop (possibly 88mt compared to 82mt this year) is in the offing for Feb/Mar next year. Argentinean farmers are still refusing to sell their soya for the same old reasons: export tax; fixed exchange rates and a hedge against inflation. Again a bigger crop is expected next harvest at 54mt compared to this year’s 50mt.

The EU feed trade is still wary of buying soya forward due to volatile pricing and volatile currency, and importers are unwilling to ship too much soya if the sales are not on the books, which could lead to tears later on. Two USDA reports, one on Monday and another on Oct 11th will provide amusement for any bored traders. Reuters believes global soya bean production will be 284mt (281mt this year).

China is still hungry. It imported about 60mt this last year, and is expected to import about 70mt this year. It is also expected to import about 10mt of wheat to make up for its appalling wheat harvest.