Drought could reduce Russian winter wheat yield

Brazil's harvest is 50% complete and major soya producing state Mato Grosso is thought to be 80% complete.

Logistical problems in Brazil are said to be ‘substantial but manageable’. The waiting ship capacity for soya is said to be 10mt. In theory the pressure on Brazil should be alleviated by early April when Argentine soya will be ready for loading.

Tenant farmers in Argentina will sell soya early, but then sales may slow as the rest will use soya as a currency and inflation hedge. In practice that gives the Brazilian port workers less than two weeks to strike for higher pay; and should mean that there will be less demand for US soya, and so less pressure underneath CBOT soya futures.

Shipments of US soya and new crop Brazilian soya have supplemented China’s dwindling port stocks; apparently almost 3mt of Brazilian soya is currently on the water heading for China.

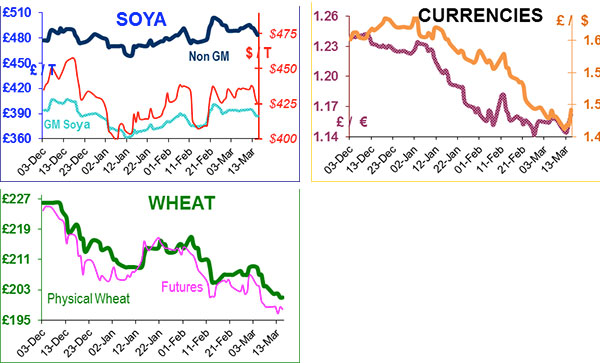

As we have commented previously, the USDA seems to have a political slant, it generally wishes to avoid issuing news which could spook the markets. So we expect a downgrade of yield to be countered with an increase in area, or a reduction of area to be negated by an increase in starting stocks.

However last Fridays’ USDA report broke new ground; it completely ignored recent (and strong) sales of soya beans, which allowed them to leave ending stocks unchanged at 125mb; presumably this is the minimum figure with which they are comfortable, the lowest carry-out for 9 years and represents only two weeks supply.

The USDA expects Brazil to produce 83.5mt of soya, and Argentina 51.5mt; a slight massaging of the figures so that world ending stocks would exceed 60mt. The Rabobank must be long of futures as it says that the Argentinian maize and soya crop has suffered ‘irreversible damage’ from hot and dry conditions.

The maize report was relatively neutral with ending stocks unchanged at 632mb, Brazilian production unchanged for this year at 72.5mt and Argentina at 26.5mt. World ending stocks were therefore slightly less than previous estimates at 117.5mt.

The Argentine maize harvest is about 20% complete. World 2012/13 wheat production lifted from 654mt to 656mt, as India is expected to produce a record 95mt this year, so world ending stocks should hit 178mt. The IGC believe that the Russian winter wheat yield will be reduced by drought and winter kill.

Russia’s priority is likely to be rebuilding of wheat stocks this year, rather than exports. The Ukraine is expected to produce a record grain crop this year –last year it exported 6.2mt of its 15.8mt wheat crop, and 13mt of its 23mt maize crop. This week the price of US wheat dipped below that of US maize, and farmers and biofuel plants are looking at using a proportion of wheat to substitute maize. As US May wheat futures are now £24/t below the UK, it would not be surprising to see some UK imports before the end of the harvest year.

Old dogs and new tricks? As the UK faces the final four months of this year, probably using a mix of crap UK wheat with Continental imports; Vietnam is allegedly mixing Indian and Australian wheat to cut costs and improve quality.